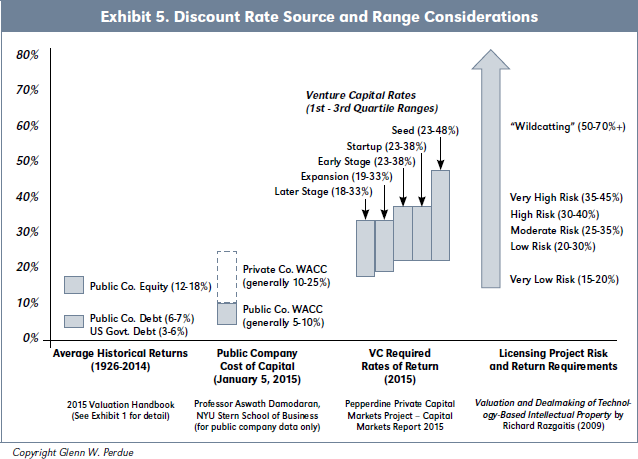

Exhibit 5 summarizes ranges of investment returns from various sources. Beyond providing context, this exhibit further illustrates how increased risk results in a logical expectation for increased returns.

The first column in Exhibit 5 summarizes average historical returns as presented in Exhibit 1 for government and public company debt (3-7 percent) and public company equity (12-18 percent). The second column in Exhibit 5 presents general value ranges for public company WACCs (5-10 percent)1 and private company WACCs (10-25 percent).2 The third column provides expected gross returns for venture capital investments for 5 stages from seed capital to later stage ventures that range from 18 percent to 48 percent. The final column summarizes licensing project return requirements developed Dr. Richard Razgaitis of 15-70 percent or more.3

Not surprisingly, the bulk of the rates cited by Dr. Razgaitis from “Low Risk” to “Very High Risk” correspond to venture capital rates, thus suggesting comparable levels of risk and expected returns. This makes sense because many venture capital investments, such as those made in Silicon Valley, are rooted in proprietary technology and intellectual property.

Based upon what’s been presented thus far, we see that certain signposts become apparent in determining an appropriate discount rate for use in financial analysis involving technology and intellectual property. These signposts are:

- The WACC which generally provides a floor value since IP and other intangible assets are generally more risky than financial and tangible assets, thus necessitating returns at or above the WACC (see Exhibit 2).

- Returns on Assets determined as part of a valuation exercise based on weighted average return analysis in which returns for IP asset groups and other intangibles are calculated (see Exhibit 3).

- The Cost of Equity which reflects the cost of “risk capital” thus corresponding more closely with the riskier assets of the business for which stand-alone debt financing may be difficult to obtain. Unlike the cost of debt which is generally based on a stated interest rate, the cost of equity is a function of market-based returns needed to compensate for the risk of holding the asset. With public companies, these returns are mediated by a fluctuating stock price.

- Venture Capital Rates which reflect rates used in funding higher-risk business ventures based on proprietary technology and intellectual property. Venture capital rates may also be appropriate for use in analyzing capital investment projects or ventures within a company that present risks greater than that of the company as a whole (e.g., the Fortune 500 company’s investment in ABC Systems as introduced in Section IV).

The above are referred to as signposts because an appropriate rate may lie between or above these published or calculable rates. And in some cases, multiple sources of information as discussed herein may be used to triangulate on an appropriate discount rate.

While the WACC was introduced in Section V, we see that the cost of equity is not only a critical component of the WACC calculation, but also an important discount rate signpost in its own right. The remainder of this section considers methods of determining a cost of equity as a consideration in the assessment of an appropriate discount rate for technology and IP-related financial analysis.

Capital Asset Pricing Model (CAPM)

As introduced in Section IV, at its most basic level, a cost of capital can be decomposed into a risk-free rate and a risk premium. The CAPM provides a way of calculating the risk premium for an individual stock or group of stocks as a function of its price volatility relative to the overall market as reflected by a variable known as “Beta.” Economist William Sharpe received a Nobel Prize for his work in this area which was presented initially in 1970. The CAPM can be stated algebraically as:

Re = Rf + (Rm - Rf)β

Where:

Re = required rate of return for the stock or group of stocks

Rf = risk-free rate of return

Rm = equity market rate of return.

(Rm – Rf) = equity market risk premium

β = beta for a specific stock or group of stocks

While the CAPM is a commonly used tool in the context of developing diversified investment portfolios, it may not produce meaningful results relevant to a cost of equity calculation for use in an IP valuation. This challenge results primarily from the manner in which Beta is used as a proxy for risk. More specifically, Beta suffers from challenges with its reliance on price volatility and correlation measures along with problems related to the historical period from which data is obtained to calculate Beta.4

Problems with the CAPM can be particularly pronounced with technology and IP-based companies that may exhibit unconventional characteristics, such as a lack of profits or even revenues as occurs with life science companies. In these cases, use of the CAPM can lead to perverse, unreliable estimates for the cost of equity.

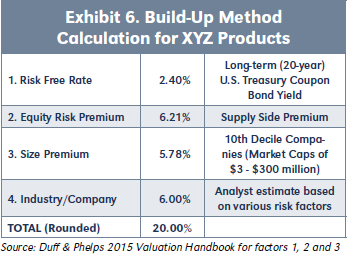

Build-Up Method

The build-up method also begins with the risk-free rate and equity risk premium but then considers additional layers of risk that, if present, form the basis for additional premiums associated with company size, the industry and the company in the general. Exhibit 6 presents a build-up method calculation example for XYZ Products:

The 20 percent cost of equity derived above is the cost of equity used in Exhibit 2 to derive XYZ’s WACC.5

The risk free rate is provided in the cited publication and can also be obtained from the St. Louis Federal Reserve for more specific periods. However, the added precision of obtaining daily or monthly rates is generally unnecessary in a technology or IP-related valuation.

As introduced in the CAPM discussion, the equity risk premium is the additional return that can be obtained above the risk-free rate by investing in public equities. Based on use of the published risk-free rate, it is generally-accepted practice to also use the supply-side equity risk premium.6

The size premium in this example was based upon the market value of equity. However, in the publication cited, book value, sales, employee count and other factors can also be used as the basis for company size and the size premium.

While certain industry premiums are also provided in the publication cited, it is common practice for industry and company premiums to be considered together in developing the final factor. This final combined premium typically ranges from 1-10 percent.

Private Capital Market Rates

Exhibit 5 presents venture capital (VC) rates ranging from 18-48 percent for five different stages of investment as detailed more fully in Exhibit 7. While the Pepperdine Survey from which these rates were obtained also provides required rates of return for other sources of private capital, Exhibit 5 focuses on VC rates due to their particular relevance in technology and IP-related financial analysis. In considering the cost of equity for an established business, rates of return sought by private equity groups (PEGs) may also be helpful.7

While venture capital firms tend to focus on younger, riskier businesses which may not have profits or even revenues, private equity groups tend to focus on established businesses with a history of both. As illustrated in Exhibit 7, PEG rates make sense when viewed in the context of later stage VC rates, but also reflect less variability.

Private equity groups may use inexpensive debt to facilitate leveraged buy-outs but seek equity-level returns as evidenced in Exhibit 7. PEGs may engage in financial engineering and strategic initiatives to aid in generating desired returns. For instance, PEGs are often involved in industry roll-ups to consolidate multiple companies within an industry to exploit economies of scale and generate cost-efficiencies. PEGs can be activist owners of traditional businesses such as manufacturing and distribution companies. In this regard, PEG rates of return may be helpful in assessing the cost of equity for a traditional business with revenues and profits, but not necessarily for a technology or IP-based business.

The appropriate venture capital rate may sufficiently capture IP-specific risks because business success in many venture-backed companies is largely based on IP and other intangibles such as proprietary software protected as a trade secret or life science technology protected through patents. In addition, the proportion of intangible assets is often very high with early-stage businesses. Since relatively few tangible assets may be present in an early-stage business, debt financing is often difficult to obtain, thus making the cost of equity a more relevant, and potentially exclusive, consideration in determining the cost of capital for technology and IP.

But even the venture capital rates identified in Exhibit 7 may not sufficiently capture the risk associated with an IP-based investment. For instance, borrowing an expression from the oil exploration industry, Dr. Razgaitis uses the term “wildcatting” to reference projects of extremely high risk for which discount rates of 50-70 percent or more may be appropriate (see Exhibit 5).

The 50 percent rate cited by Dr. Razgaitis coincides with the 48 percent third-quartile seed rate for venture capital. Dr. Razgaitis references a start-up company going 3into business to make a product not presently sold or even known to exist using unproven technologies to characterize this type of risk, a characterization consistent with that of a seed capital investment. Keep in mind, the 48 percent seed capital rate is a third quartile rate meaning that another 25 percent of the observations in the sample were above this level and thus reached deeper into the 50-70 percent range cited by Dr. Razgaitis.