Robert L. Vigil

Principal

Analysis Group, Inc.

Washington, D.C.

Robert L. Vigil

Principal

Analysis Group, Inc.

Washington, D.C. Xiao Zhang

Associate

Analysis Group, Inc.

Washington, D.C.

Xiao Zhang

Associate

Analysis Group, Inc.

Washington, D.C.In patent infringement cases, there is often a need to rely upon patent license agreements and patent sale agreements to determine the royalty that the alleged infringer should pay for using the patent-in-suit. When the payment in the license or sale agreement reflects compensation for more than the patent-in-suit, it may be necessary to apportion the royalty or price to account for the value attributed to the other patents in the portfolio. In order to account for the well-known disproportionality of patent values, we propose the use of information from various patent value distribution studies to aid in this apportionment. This paper summarizes the literature related to patent value distributions and provides a framework for how these distributions may be used in patent litigation to apportion patent value from license or sale agreements.

Experts in patent infringement cases frequently rely upon patent license agreements and patent sale agreements to determine the royalty that the alleged infringer should pay for using the patentin- suit. This is possible when the agreement transfers rights to the patent-in-suit or when it transfers rights to another patent that is technically comparable to the patent-in-suit. In situations where the license or sale agreement involves only, or primarily, the patent-insuit or a technically comparable patent, use of these agreements is usually simple and straightforward. In other situations, however, when the license or sale agreement transfers rights to a large portfolio of patents, using these agreements to determine the value of just the patent-in-suit can present challenges. In situations where the royalty or price paid in these agreements does not reflect compensation for just the patent-in-suit or a technically comparable patent, in order for the license or sale agreement to provide probative evidence regarding the value of just the patent- in-suit, it often is necessary to apportion the royalty or price from the agreement to account for the other patents included in the portfolio.1 Because of well-established research that shows that patent values are highly skewed,2 this apportionment can rarely be achieved by merely dividing the royalty or price in the agreement by the number of patents in the portfolio.3

One method that may be used to apportion the royalty or price paid in these agreements, which accounts for the disproportionality of patent values, relies upon information from academic research regarding the distribution of patent values for different groups of patents. This research, which utilizes a range of methodologies and a variety of data for different time periods and different countries, provides information about how much of the total value from different groups of patents come from one or more patents within the group, i.e., how much of the total value of all electronics patents comes from the top 10 percent of patents. This information can then be combined with information about the relative value of the patent-in-suit or technically comparable patent compared to other patents in the portfolio to apportion the royalty or price in the agreement.

The purpose of this article is to summarize relevant academic research that provides insight into the distribution of patent values and to discuss how the results from this research may be used to apportion the royalty or price paid in portfolio license and sale agreements. In Section II, we summarize the literature related to patent value distributions; in Section III, we provide a framework for how these distributions may be used in patent litigation to apportion patent value from license or sale agreements; and in Section IV, we offer some general conclusions and observations.

A. Distributions Based on Patent Renewals

Several researchers have used patent renewals to study the value of patents.4 What makes this kind of analysis possible is that patent holders need to pay renewal fees, which usually increase over time, in order to keep patent protection in force.5 The underlying premise of the patent renewal research is that patentees compare the return to patent protection to the cost of maintaining that protection and respond optimally by either paying the renewal fees to renew the patents or not paying the renewal fees and letting the patents lapse.6

This is consistent with general economic theory, which holds that individuals and companies will invest in an asset only if the expected economic benefits generated by the asset exceed the expected investment required to obtain or maintain the asset, taking into account relevant risk factors, anticipated rates of return, and other considerations.7 Hence, a rational patent owner should choose to pay the maintenance fees for a patent only if it believes the expected future stream of benefits from that patent exceed the cost of the maintenance fees.8 As a result, the length of a patent’s life, and in particular the amount of maintenance fees that were or were not paid for that patent, reveals relevant information about the expected value of the patent to its owner—assuming rational economic decision- making.9

This section provides a summary of some of the more frequently cited studies on patent renewals. These studies generally reflect the findings in the literature on this subject.

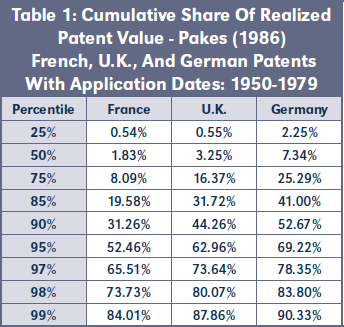

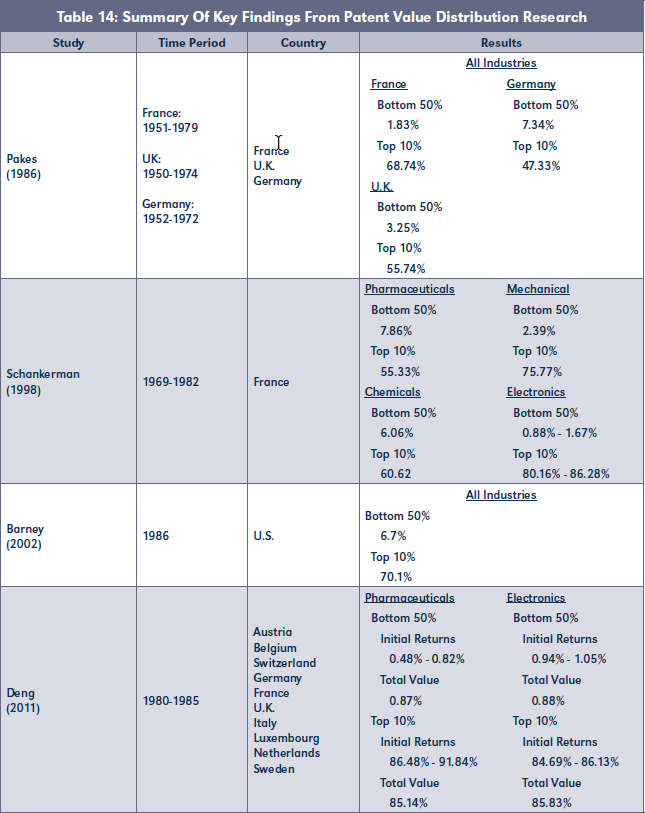

Pakes (1986)

Pakes (1986) utilized observations on the proportions of different cohorts of patents which are renewed at alternative ages, together with the relevant renewal fee schedules, to determine the distribution of patent values and the evolution of these distributions over the lifespan of the patents.10 This research was based upon all French patents applied for between 1951 and 1979, all U.K. patents applied for between 1950 and 1974, and German patents granted from applications between 1952 and 1972.11 Table 1, below, summarizes the cumulative shares of realized patent values reported by Pakes (1986) for each percentile.12 These results suggest that the bottom 50 percent of patents in France, the U.K., and Germany account for 1.83 percent, 3.25 percent, and 7.34 percent of the total realized value, respectively. The top 10 percent of patents comprise 68.74 percent, 55.74 percent, and 47.33 percent of the total value of patents in these countries, respectively. The distributions in all countries, though different, are all highly skewed.13

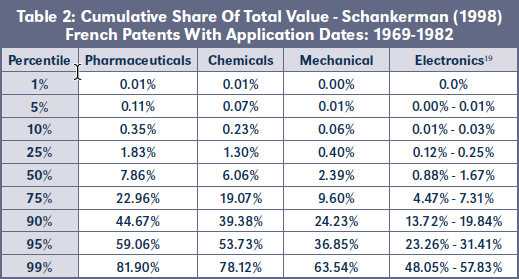

Schankerman (1998)

In his article, “How Valuable is Patent Protection? Estimates by Technology Field,” Schankerman (1998) utilized patent renewal data for nearly all patents applied for in France during the period 1969-1982 to estimate the private value of patent rights in the following four technology fields: pharmaceuticals, chemicals, mechanical, and electronics.14 The main empirical findings of Schankerman (1998) are that the distribution of the private value of patent rights is highly skewed in all technology fields, with most of the value concentrated in a relatively small number of patents in the right tail of the distribution.15 Schankerman (1998) found that, for all four technology groups studied, the lognormal distribution fit the data better than other distributions tested.16 Schankerman (1998) provided a summary of patent values for the different technology groups at six different quantiles which showed that most patents have very little private value and that the value rises sharply with the quantile, especially for mechanical and electronics patents.17

Using the results in Schankerman (1998), one can estimate the share of value that comes from patents at each percentile in the distribution and the cumulative share that comes from different groups of patents. To estimate these shares, we created a set of patent values for each percentile in the distribution and calculated each percentile’s share of the total value. The patent values at each percentile were estimated by simulating a lognormal distribution that fits the reported 95th and 99th percentiles of the distribution of patent values reported in Schankerman (1998). Specifically, we generated a simulated set of patent values, Vi, based upon one million random draws of Xi from a standard normal distribution such that:

Vi = exp(μ+(σ×Xi ),with Xi~N(0,1)

Note that μ and σ in the above equation can be determined by solving the following simultaneous equations:

V95= exp(μ+(σ×U95))

V99= exp(μ+(σ×U99))

where V95 and V99 are the 95th and 99th percentiles of value reported by Schankerman (1998) and U95 and U99 are the results of the inverse normal functions evaluated at 0.95 and 0.99, respectively. Using the electronics (excluding Japan) category as an example, V99 = 481,429 and V95 = 113,403, yielding μ = 8.14625 and σ = 2.12307.

Based upon the shares estimated for each percentile in the distribution, we calculated the cumulative shares for different groups of patents in the distribution and report this information in Table 2.18 As Table 2 shows, the distribution of patent values in all technology fields is highly skewed. For example, the bottom 50 percent of pharmaceutical, chemicals, mechanical, and electronics patents comprise 7.86 percent, 6.06 percent, 2.39 percent, and 0.88 - 1.67 percent of the total value of patents in these technology categories, respectively. The top 10 percent of patents account for 55.33 percent, 60.62 percent, 75.77 percent, and 80.16 percent - 86.28 percent of the total value of pharmaceutical, chemicals, mechanical, and electronics patents, respectively. Though there is significant skew across all technology fields, there are differences across technology groups. As observed by Schankerman (1998), these differences fall into two categories: in the pharmaceuticals and chemicals fields, the value distributions are characterized by relatively low mean and dispersion, and slow rates of depreciation; for mechanical and electronic patents, the value distributions are characterized by a higher mean value, greater dispersion, and faster depreciation.20

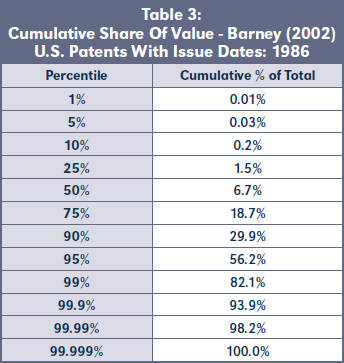

Barney (2002)

Barney (2002) examined the value distribution of U.S. patents by analyzing the survival rates of approximately 70,000 U.S. patents issued in 1986.21 Using the abandonment rates of these patents, together with the escalating maintenance fees that are required of U.S. patents, Barney (2002) estimated the value contributions of the patents, by percentile.22 The cumulative share of value by percentile implied by these results is shown in Table 3. These results suggest that the bottom 50 percent of patents represent 6.7 percent of the total value of the patents and that the top 10 percent of patents account for 70.1 percent of the total value of the patents. These results “support the view, long held by many in the field, that patent values are highly skewed. A relatively large number of patents appear to be worth little or nothing while a relatively small number appear to be worth a great deal.”23

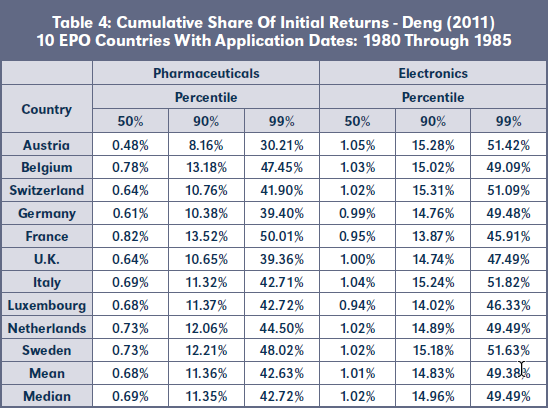

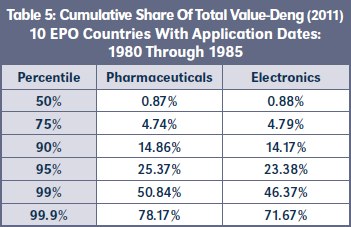

Deng (2011)

Deng (2011) developed a joint patent renewal and patent application model to estimate the distribution of patent values of pharmaceutical and electronics patents whose applications were submitted to the European Patent Office (“EPO”) between 1980 and 1985.24 Using this model, Deng (2011) obtained information on the distribution of patent values in the following EPO member countries: Austria, Belgium, Switzerland, Germany, France, U.K., Italy, Luxembourg, Netherlands, and Sweden.25 Table 4 shows the cumulative distributions of the initial returns for each technology field across countries for the 50 percent, 90 percent, and 99 percent percentiles, as reported by Deng (2011).26

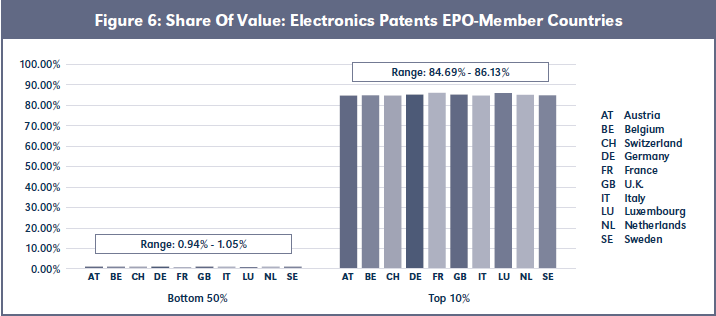

As Table 4 shows, Deng (2011) found that, across all countries and technology categories, the distribution of initial patent returns is highly skewed.27 Across countries, the initial returns of the bottom 50 percent of pharmaceutical patents and electronics patents comprise between 0.48 percent - 0.82 percent and 0.94 percent - 1.05 percent of the total initial returns for these technologies, respectively. The top 10 percent of pharmaceutical patents and electronics patents comprise between 86.48 percent - 91.84 percent and 84.69 percent - 86.13 percent of the total initial returns across countries for these technologies, respectively. There is very little difference in the mean and median of cumulative initial returns across countries for both technology categories and all three percentiles.

The highly skewed nature of patent values can also be seen by examining the value distribution of the patent families over their whole lives (as opposed to the value distribution of the initial returns).28 As Table 5 shows,29 across all 10 EPO member countries,30 the bottom 50 percent of pharmaceutical and electronics patents comprise less than 1 percent of the total value; the top 10 percent of pharmaceutical and electronics patents account for 85.14 percent and 85.83 percent of patents in these technology categories, respectively.

B. Distributions Based on Surveys and Licensing Royalties

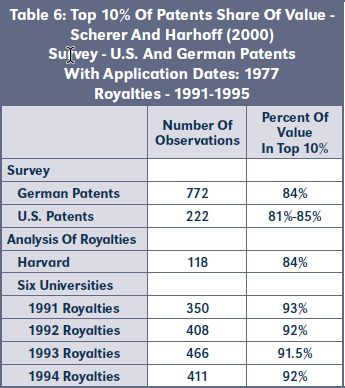

Scherer and Harhoff (2000)

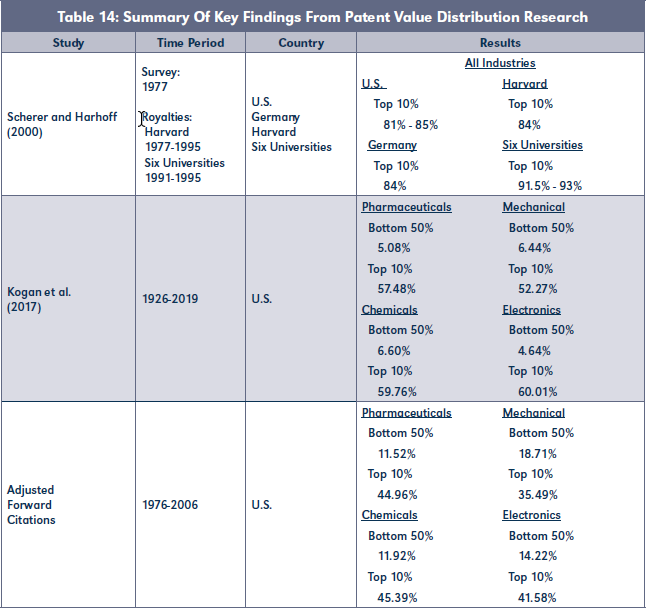

In order to assess the distribution of patent values, Scherer and Harhoff (2000) conducted two analyzes. First, they performed a survey of owners of German patents that resulted from German patent applications filed in 1977 and owners of related U.S. patents.31 As part of the survey, respondents were asked to identify the smallest amount that they would have been willing to sell each patent for, had they possessed full knowledge of the profit potential of the patent.32 Respondents subsequently placed each patent in one of five value categories ranging from less than DM 40,000 to more than DM five million.33

Second, as part of their assessment of the distribution of patent values, Scherer and Harhoff (2000) examined a) the royalties received between 1977 and 1995 on 118 patent “bundles” covering inventions made by Harvard University employees and licensed by the Harvard Office of Technology Licensing, and b) the royalties received between 1991 and 1995 on inventions made at six research-oriented U.S. universities.34 These royalties were used to assess the relative value of each patent and the distribution of patent values within each group.

Their research revealed “a high level of confidence that the size distribution of private value returns from individual technological innovations is quite skewed— most likely adhering to a log normal law. A small minority of innovations yield the lion’s share of all innovations’ total economic value.”35 Table 6 shows the proportion of total value realized by the top 10 percent of patents reported by Scherer and Harhoff (2000).

These results suggest that 84 percent of the value of the German patents and 81 to 85 percent of the value of the U.S. patents comes from the top 10 percent of patents studied. Their results also suggest that 84 percent of the royalties from the Harvard patents and between 91.5 percent and 93 percent of the royalties from the six research universities come from the top 10 percent of patents.

C. Distributions Based on Stock Price Movements

Event study methodologies are some of the most frequently used analytical tools in financial research.36 Event studies seek to find the abnormal returns attributable to the event being studied by adjusting for the return that is attributable to the price fluctuation of the market as a whole.37 One common variant of this methodology estimates what the “normal” stock re- turn of the affected firm would have been during the event window, absent the event, by using an estimation window prior to the event. Thereafter, the method deducts this “normal” return from the “actual” return to identify the “abnormal” return attributed to the event.38 The event being studied often is related to the release of information to market participants through the financial press.39

Originally developed as a statistical tool for empirical research in accounting and finance, event studies have become common in numerous other disciplines as well, including economics, history, law, management, marketing, and political science.40 The idea that stock market fluctuations can be linked to patent value is not new.41 Event studies have been used by several researchers to try to disentangle the value of patents from changes in stock prices following news about patents. While there is research that links patent value to stock price movements, we are unaware of any papers, other than Kogan et al. (2017), that report the patent values that were estimated as part of the studies.

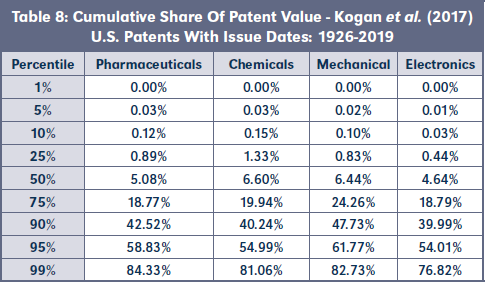

Kogan et al. (2017)

Kogan et al. (2017) estimated the private value of U.S. patents using stock market responses to news about patents.42 They focused on patents granted over the period 1926 to 2010 whose assignee could be matched to public companies for which stock price information could be obtained.43 Kogan et al. (2017) analyzed stock price movements during a three-day announcement window beginning the day the patent issued.44 Because stock prices may have fluctuated during the announcement window for reasons unrelated to the patents, they isolated each firm’s idiosyncratic return related to the patent’s issuance—defined as the firm’s return minus the return on the market portfolio.45 Kogan et al. (2017) estimated the value of each patent as the product of the estimate of the stock return due to the value of the patent and the market capitalization of the firm that was assigned the patent.46 Kogan et al. (2017) report that “the resulting distribution of the estimated patent values is fat-tailed, consistent with past research.”47

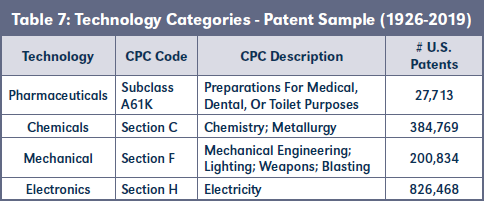

The authors provided subsequent patent value estimates using updated data on U.S. patents issued from 1926 to 2019 that were calculated using the same methodology described in Kogan et al. (2017).48 This updated data included patent values for 2.8 million U.S. patents. We merged the information on patent values obtained from these updated data with information from the United States Patent and Trademark Office (USPTO) regarding the primary Cooperative Patent Classification (CPC) code assigned to each patent.49 Using these data, we estimated the patent value distributions for groups of patents in different CPC categories. In choosing which groups of patents in the CPC to analyze, we sought to study the same technology classifications in Schankerman (1998)—namely pharmaceuticals, chemicals, mechanical, and electronics.

Toward that end, for the pharmaceutical sector, we used all patents in Subclass A61K of Class A61 of Section A of the CPC;50 for the chemicals sector, we used all patents in Section C of the CPC; for the mechanical sector, we used all patents in Section F of the CPC; and for the electronics sector, we used all patents in Section H of the CPC. Table 7 provides the CPC descriptions and the number of patents in our sample for each of these four technology categories. Kogan et al. (2017) reported both nominal values and real values, which were deflated to 1982 dollars using the Consumer Price Index. In order to control for the impact of inflation on patent values, we based our analysis on real values. Using these values, we calculated the cumulative patent value shares for each of these technology categories. These shares are shown in Table 8 for different percentiles in the distribution.

As these data show, the cumulative patent value distributions for patents in these technology classes exhibited significant skew. For example, the bottom 50 percent of pharmaceutical, chemicals, mechanical, and electronics patents comprise 5.08 percent, 6.60 percent, 6.44 percent, and 4.64 percent of the total value of patents in these technology categories, respectively. The top 10 percent of patents account for 57.48 percent, 59.76 percent, 52.27 percent, and 60.01 percent of the total value of pharmaceutical, chemicals, mechanical, and electronics patents, respectively. While these patent value distributions differ across technology categories, the differences appear to be less than those suggested by Schankerman (1998).

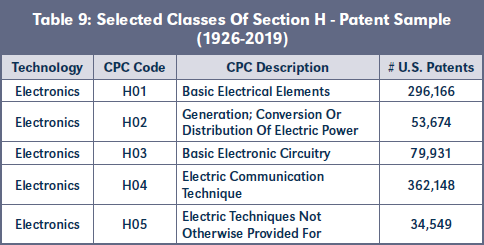

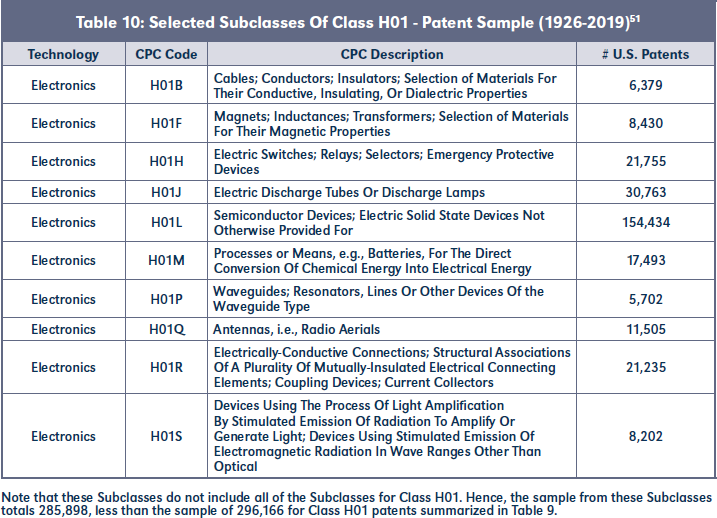

While we have attempted to use the same technology categories as Schankerman (1998), it is not clear how similar the CPC technology categories that we utilized are to the technology categories used by Schankerman (1998). It is possible that the Schankerman (1998) categories are more or less broad, or just different, than those used in our analysis. In order to analyze the sensitivity of our results to our selection of CPC technology category (i.e., how broad or narrow the category is defined), we compared the patent value distributions for CPC Section H (Electricity) with those for the five main CPC classes of Section H (Classes H01, H02, H03, H04, and H05) and the 10 main CPC Subclasses of Class H01 (H01B, H01F, H01H, H01J, H01L, H01M, H01P, H01Q, H01R, and H01S). Tables 9 and 10 provide descriptions and the number of patents in our sample for each of these CPC technology categories.

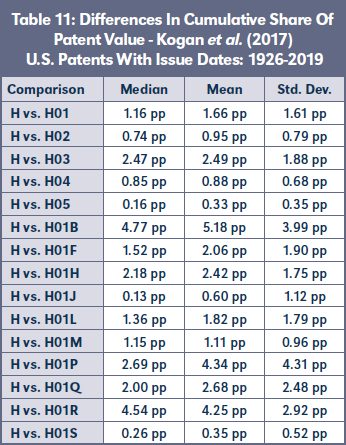

One way to analyze the similarity in the distributions of patent values for these various groups of patents is to examine the difference in cumulative shares of value for each group of patents at each percentile in the distribution. We compared the cumulative share of value at each percentile of the distribution for all patents in Section H with that of each of the five main, 3-digit Classes of Section H and each of the 10 main, 4-digit Subclasses of Class H01. Table 11 shows descriptive statistics regarding the percentage point difference in cumulative shares of value between these various groups of patents.52

As this table shows, the mean and median difference in the cumulative share of value between patents in Section H and patents in the various subcategories of Section H, across percentiles, is relatively small. For example, the median difference, across percentiles, in the cumulative share of value for patents in Section H compared to patents in the five main classes in Section H was between 0.16 and 2.47 percentage points. The mean difference was only slightly higher. This provides at least some evidence that patent value distributions are generally consistent across categories containing patents that are in the same broad technology field. It also may suggest that the results in Table 8 may not be particularly sensitive to the Classes or Subclasses that are used to define the four main technology categories that we analyzed.

These results suggest that patent value distributions related to patents that are part of a broad measure of technology may be used to reliably estimate the patent value distributions of groups of patents that comprise narrower subsets of the broader technology. In other words, the distribution of value of electronics patents, as an example, may be a reliable indicator of the distribution of value of groups of specific types of electronics patents, such as semiconductor patents.

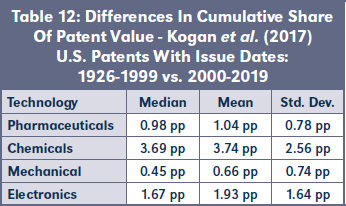

We also examined whether there is a significant difference between the distribution of patent values estimated by Kogan et al. (2017) based on the time period of the patents analyzed. Specifically, for each of our four main technology categories (pharmaceuticals, chemicals, mechanical, and electronics), we analyzed the difference in cumulative shares of value between patents that had issued between 1926 and 1999 and patents that had issued between 2000 and 2019.53 For the pharmaceuticals, chemicals, mechanical, and electronics categories, approximately 56 percent, 27 percent, 37 percent, and 67 percent of the patents were issued in the 2000 to 2019 time period. The results of this analysis are shown in Table 12.

As Table 12 shows, while there are differences in the cumulative share of value based on the time period studied, these differences are not dramatic. While patent values in the U.S. for these technologies may have changed over time, patent value distributions have been relatively stable. This suggests that patent value distributions related to patents issued in one time period may be used to reliably estimate the patent value distribution of patents issued in another time period.54 In other words, the distribution of value of electronics patents issued between 1969 and 1982, as an example, may be a reliable indicator of the distribution of value of electronics patents issued in 2010.

Kogan et al. (2017) note that their patent value estimates “seem a bit high” and that one possible explanation for this is that their estimates are based upon a sample of patents owned by public firms and that public firms may attach a higher value to patents than non-public firms.55 We have not seen definitive support, however, for the proposition that patents owned by public companies are systematically more valuable than patents not owned by public companies. Moreover, even if that were the case, this would introduce selection bias into the sample only if the patent value distributions for patents owned by public companies are different than those not owned by public companies.56

D. Distributions Based On Patent Citations

Forward patent citations occur when a patent is cited by subsequently issued patents.57 The number of forward patent citations is considered an important indicator of scientific and technical significance and, according to many researchers, can serve as a valid measure of economic value.58 Harhoff et al. (1999) identified at least two reasons for this. First, “it is reasonable to suppose that the prior inventions cited in new patents tend to be the relatively important precursors that best define the state of the art. The broader the shoulders, the more likely they are to be cited.”59 Second, “because prior inventions set the stage for new inventions, citations are used to measure a potentially important economic externality, i.e., the impact the knowledge embodied in prior inventions has in stimulating new contributions.”60

Numerous researchers have found that there is a positive correlation between economic value and the number of forward citations—more economically valuable patents tend to be more heavily cited.61 For example, previous research has found correlations between patent citations and various measures of economic value inferred from things such as patent owner surveys, firm market value, licensing fees, stock market reactions to patent grants, and patent renewal rates.62 According to Malaspina (2019), the basic intuition behind this correlation is that “valuable patented technology will encourage new yet related innovations, which will increase the number of citations back to the prior patented technology thereby increasing the citation counts of the prior patented technology.”63 Hall et al. (2005) noted that because “[p]atented innovations are for the most part the result of costly R&D conducted by profit-seeking organizations; if firms invest in further developing an innovation disclosed in a previous patent, then the resulting (citing) patents presumably signify that the cited innovation is economically valuable.”64

While there is general consensus that there is a positive correlation between patent citations and patent value, the correlation is not perfect.65 Various studies have found that “the value-citation relationship is quite noisy.”66 Though some researchers have found the relationship between patent citations and patent value to be linear, others have found it to be more complex and non-monotonic.67 Some have suggested that patent citations are a better proxy for the value of lower valued patents than higher valued patents.68 Others have argued that patent citations may be a more meaningful measure of the value of the underlying technology than of the quality of patents themselves.69 All of this notwithstanding, most agree that there is a positive relationship between patent citations and patent value and that forward patent citations are a meaningful, albeit imperfect, predictor of patent value.

Experts have relied upon, and courts have accepted, the use of forward citation analysis to estimate the relative value of patents contained in license and sale agreements.70 For example, the Court in Mfg. Res. Int’l, Inc. v. Civiq Smartscapes, LLC stated that “[f]orward citation analysis has an academic pedigree that supports it as a reliable methodology” and that “[f]orward citation analysis can be a reliable method to decide the relative value of patents and to assist in determining a reasonable royalty.”71 In Comcast Cable Commc’ns, LLC v. Sprint Commc’ns Co., the Court ruled that “forward citation analysis is reliable” for corroboration of a damages opinion.72 In Evolved Wireless, LLC v. Apple Inc., the Court found that the “citation analysis method has generally been regarded as reliable” for estimating the value of patents.73 In cases where courts have found forward citation to be unreliable, it was not because of the methodology, per se, but because the application of the methodology did not account for the facts of the case.74

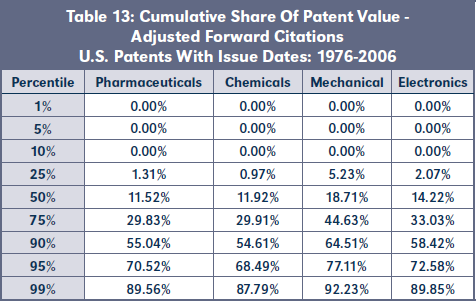

Because patent citations provide some measure of patent value, we examined the distribution of forward citations for patents in the same technology classifications in Schankerman (1998): pharmaceuticals, chemicals, mechanical, and electronics. As with our analysis of Kogan et al. (2017), for the pharmaceutical sector, we analyzed citations of all patents in Subclass A61K of Class A61 of Section A of the CPC; for the chemicals sector, we analyzed citations of all patents in Section C of the CPC; for the mechanical sector, we analyzed citations of all patents in Section F of the CPC; and for the electronics sector, we analyzed citations of all patents in Section H of the CPC. In total, we analyzed citations for 39,839 patents, 383,046 patents, 247,497 patents, and 507,767 patents in CPC codes A61K, C, F, and H, respectively.

In order to estimate the forward citation distributions for these groups of patents, we obtained patent citation counts from the NBER U.S. Patent Citations Data File.75 These data contain information on 3,210,361 utility patents granted by the USPTO from 1976 to 2006.76 Among other things, for each patent, the NBER U.S. Patent Citations Data File provides information on the patent number, the grant date, and the number of U.S. citations. We mapped these data to the patents in each of our four CPC technology classifications by merging the data with information from the USPTO regarding the primary CPC code assigned to each patent.

To calculate the number of forward citations for each patent in each of the four different groups of patents described above, we adjusted the number of citations for both the age and technology of the patent.77 Controlling for age and technology when analyzing patent citations is well-documented in both the academic literature and patent litigation.78 A patent’s age may bias its forward citation count because, as the time since the patent issued increases, there are more opportunities for the patent to accumulate forward citations from subsequently issuing patents. Similarly, a patent’s field of technology may affect its forward citation frequency because patents from different fields of technology may accumulate citations at fundamentally different rates.79

We adjusted the number of citations for age and technology by dividing the number of raw citations for each patent by the median number of citations of patents in the same IPC code granted within six months before or after the grant date of each patent.80 This is similar to the “fixed-effects” approach suggested by Hall et al. (2001).81 As Hall et al. (2001) note, this approach treats a patent that received 11 citations and belongs to a group in which the average patent received 10 citations as equivalent to a patent that received 22 citations, but happens to belong to a group in which the average was 20. Similarly, such a patent would be regarded as inferior to a patent receiving just three citations but for which the group average was only one. One advantage of this approach is that it does not require one to make any assumptions about the underlying processes that may be driving differences in citation intensities across groups.82

Using this methodology, we calculated the number of adjusted forward citations for each patent in the four technology categories. Table 13 shows the cumulative share of adjusted citations for patents in each category at different percentiles in the distribution.

As this table shows the bottom 50 percent of pharmaceutical, chemicals, mechanical, and electronics patents comprise 11.52 percent, 11.92 percent, 18.71 percent, and 14.22 percent of the adjusted citations of patents in these technology categories, respectively. The top 10 percent of patents account for 44.96 percent, 45.39 percent, 35.49 percent, and 41.58 percent of the adjusted citations of pharmaceutical, chemicals, mechanical, and electronics patents, respectively. These data show that the distributions of adjusted citations for patents in these technology classes exhibited significant skew—though much less than distributions based on patent renewals, surveys, royalties, and stock price movements.

E. Summary

Table 14 summarizes some of the key findings from each of the studies discussed above.

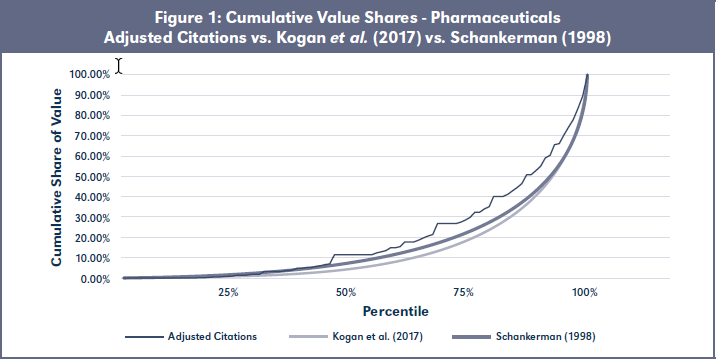

Several observations about these studies can be made. First, though the data and methodology used in these studies are different, their results generally corroborate the conclusion that patent values are highly skewed, with most of the value concentrated in a relatively small number of patents at the right tail of the distribution. This is evident from each study, regardless of its time period, geography, methodology, or technology of the patents examined.

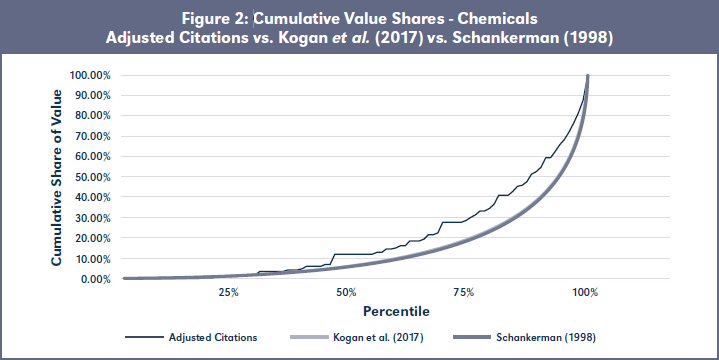

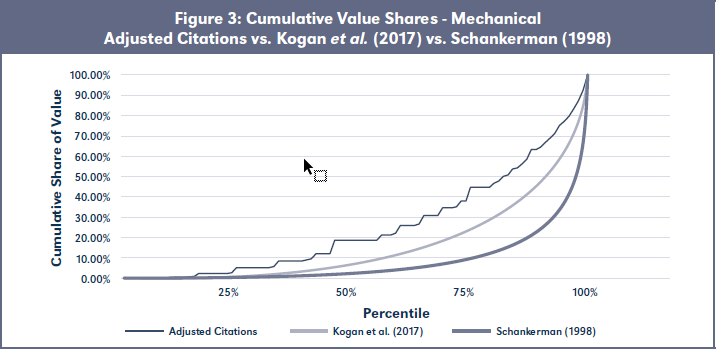

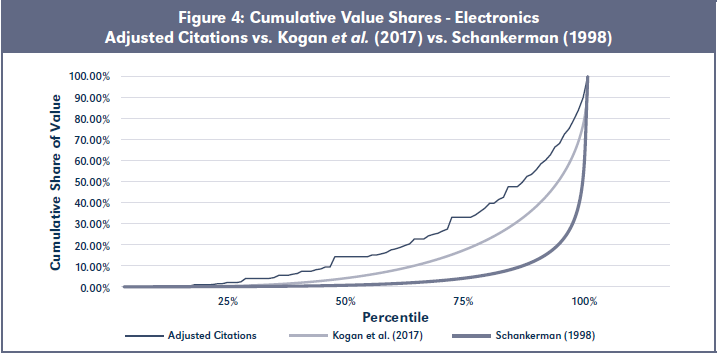

Second, the degree of disproportionality of patent values indicated by these studies is different, depending upon the methodology used. This is evident from Figures 1-4, which compare the cumulative value shares based upon adjusted citations, stock price movements (i.e., Kogan et al. (2017)), and patent renewals (i.e., Schankerman (1998)). As these figures show, the differences in cumulative value shares are greater for some technologies more than others and for some methodologies more than others.

These differences do not necessarily mean that the individual patent value distributions from the various studies are invalid or that there is a problem with the underlying valuation methodologies. Rather, these differences more likely reflect the fact that each methodology is measuring different things or looking at value in different ways. For example:

Each of these value measures is valid and reliable for the information they convey. Because the value distributions from these different methodologies are measuring different things, a comparison of the distributions may not be particularly probative. Each measure provides relevant, albeit different, information about the range of values that may be associated with the patents. Each should be considered and given their appropriate weight. How relevant a particular measure is for a given case may be different depending upon the facts and circumstances of the case, including the nature of the patent portfolio being examined, what other information is known about the patents in the portfolio, and how the patent value distributions will be used.

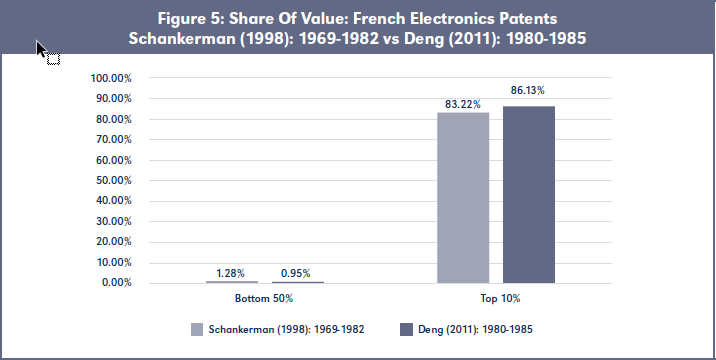

Comparing the patent value distributions for a given methodology suggests some similarity in distributions across studies, at least for certain technology categories. For example, the degree of disproportionality in patent values for patents in the electronics field reported by Schankerman (1998) is consistent with the disproportionality found in Deng (2011) for other time periods, for the same country.84 For example, Figure 5 on page 258 shows a comparison of the share of patent value that comes from the bottom 50 percent and the top 10 percent of French patents at two different time periods—Schankerman (1998): 1969–1982 and Deng (2011): 1980–1985.85 As this figure shows, the shares of value for these French electronics patents are very similar in these two different time periods.

The degree of disproportionality of French patent values reported by Schankerman (1998) and Deng (2011) is similar to the disproportionality found by Deng (2011) for electronics patents from other countries. For example, Figure 6 on page 258, shows a comparison of the shares of patent value that come from the bottom 50 percent and the top 10 percent of electronics patents in the 10 different EPO-member countries.86 As this figure shows, the shares of value for these electronics patents are very similar across countries.

While the degree of disproportionality in patent values for patents in the electronics field reported by Schankerman (1998) is consistent with the disproportionality found for electronics patents in other time periods and other countries, as reported by Deng (2011), the degree of similarity for other technology fields is less clear. For example, the shares of value reported by Schankerman (1998) and Deng (2011) for French pharmaceutical patents in 1969-1982 vs. 1980-1985 are less similar, though both distributions still reflect a high degree of skew.87 There is, however, some evidence that the degree of disproportionality in patent values in the pharmaceutical field is similar across countries.88 There is no basis to compare the shares of value reported by Schankerman (1998) for the chemicals and mechanical fields, as no other study separately examined patents in these technology fields.

The results from these studies also suggest that patent value distributions related to patents that are part of a broad measure of technology may not be materially different from distributions related to groups of patents that comprise narrower subsets of the broader technology. These studies also suggest that, for a given technology, patent value distributions have been relatively stable over time and may not be materially different across countries. All of this suggests that the results discussed above may be generalizable to a greater set of facts and circumstances than those fitting the data used in the individual studies.

In certain circumstances, information from patent value distributions may be useful in patent litigation cases to apportion patent values from license or sale agreements which contain the patent-in-suit, or a technically comparable patent, and other patents.89 These distributions may play a role in the apportionment analysis required by courts, which requires that reasonable royalty damages be based only on the incremental value of the patented invention and not on other contributions.90 This is relevant when analyzing license or sale agreements because the agreement upon which the reasonable royalty is based may convey rights to more than just the patent-in-suit or the technically comparable patent. In these situations, the royalty or price in these agreements must be apportioned to reflect the portion attributable to the patent at issue.91

Toward this end, the results from patent value distributions may be useful for this type of apportionment exercise.92 As a starting point, use of these distributions requires information about where the patent at issue ranks in comparison with other patents in the portfolio. In some cases, this information may be obtained from the technical expert (i.e., the technical expert may opine that the patent at issue is in the top 10 percent of the patents in the agreement).93 In other cases, this information may be obtained from other analyzes, such as forward citation analysis, which ranks patents in the agreement based on citations. In certain situations, experts may simply offer a counterfactual assumption about where the patent ranks (i.e., defendant’s expert may “conservatively” assume the patent is in the top 10 percent of patents despite evidence that it is a lower-valued patent).

Information about a patent’s ranking among other patents in the agreement may be combined with results from patent value distributions to apportion the royalty or price paid in the agreements.94 For example, if there was evidence that a patent was in the top 10 percent of patents in a portfolio in a license or sale agreement, one could rely upon the cumulative value shares discussed above to determine how much of the royalty or price paid in the agreement is attributable to the top 10 percent of patents. By way of illustration, if a portfolio of patents in the agreement were electronics patents, the results from Schankerman (1998), Deng (2011), and Kogan et al. (2017) would suggest that the top 10 percent of patents in the portfolio would account for between 60.02 percent and 86.28 percent of the royalty or price specified in the agreement.

Because the patent of interest is often not the only patent in the top 10 percent of patents, the expert must further apportion the royalty or price to account for these other patents. For example, if the agreement contained 100 patents, only one of which was the patent at issue, the top 10 percent of patents would include 10 patents. This further apportionment can be accomplished in a number of ways, such as reliance upon the opinion of a technical expert or a forward-citation analysis of the patents in the top 10 percent of the portfolio. Sometimes, experts may simply make an assumption about the relative value of the patents in the top 10 percent, such as that all patents in the top 10 percent of patents have equal value.95 Other times, when the testimony is on behalf of the defendant, experts may “conservatively” assume that all of the value apportioned to the top 10 percent of patents comes from the patent at issue.

In another variant of this methodology, experts may use the results from forward citation analysis along with patent value distributions from patent renewals or stock price movements to apportion the royalty or price paid in license and sale agreements. For example, in one method discussed by Malaspina (2019),96 forward citation analysis is used to determine where the patent at issue and other patents in the portfolio rank among patents in the same or a similar field (e.g., in which percentile each of the patents falls among all electronics patents). Experts then match the percentile rankings for each patent in the portfolio from the forward citation analysis, with the patent values from Schankerman (1998), Deng (2011), or Kogan et al. (2017) that correspond to the same percentile rankings in their analysis. The patent values assigned to each of the patents in the portfolio are then used to obtain relative valuations for each of the patents in the portfolio.97

Patent value distributions based on forward citation analysis also may be used to apportion patent values from license and sale agreements by themselves, without combining them with distributions based on some other method, as Malaspina (2019) suggests. As noted above, experts have sought to apportion the royalty or price paid in license or sale agreements by using only the distribution of forward citations of patents that are in the agreement under consideration. Under this method, the expert uses the forward citation distribution to determine the relative value of the patentin- suit, or technically comparable patent, compared to all other patents in the agreement. For example, if the patent-in-suit represented 10 percent of all forward citations associated with the patents in the agreement, the expert would apportion 10 percent of the royalty or price to the patent-in-suit.

In addition to using patent value distributions to apportion the royalty or price paid in license and sale agreements, these patent value distributions may also be used to determine the portion of a product’s profits that may be attributable to a patent or set of patents.98 For example, in one case, under the assumption that the patents of interest were in the top 10 percent of all 802.11 standard-essential patents, an expert multiplied the profit margin on a Wi-Fi chip by 84 percent, which is the cumulative share of value attributable to the top 10 percent of electronics patents from Schankerman (1998).99 To determine how much of the value attributable to the top 10 percent of patents was from the patents at issue, the expert multiplied that value by the proportion of the top 10 percent of patents accounted for by the patents at issue (implicitly assuming that all patents in the top 10 percent were equally valuable).100

In patent infringement cases, there is often a need to rely upon patent license agreements and patent sale agreements to determine the royalty that the alleged infringer should pay for using the patent-in-suit. Problems arise, however, when the payment in the license or sale agreement reflects compensation for more than the patent-in-suit, or another patent that is technically comparable to the patent-in-suit. In these cases, in order for the license or sale agreement to provide probative evidence regarding the value of just the patent-insuit or technically comparable patent, it is necessary to apportion the royalty or price to account for the other patents in the portfolio.

In most cases, because of research showing that patents in a portfolio are unlikely to have equal value, this apportionment is rarely achieved by merely dividing the royalty or price by the number of patents in the portfolio. Another method that may be used, which takes into account the well-known disproportionality of patent values, involves the use of information from patent value distributions. Experts may use the value distributions derived from one or more different methods to estimate the distribution of values of patents contained in license or sale agreements, which could then be used to determine the proportion of the total royalty or price paid in the agreements that may be potentially attributable to the patent-in-suit or the technically comparable patent.

In this paper, we have summarized the patent value distributions from studies that used different methodologies and different data. These studies suggest that patent value distributions related to patents that are part of a broad measure of technology may not be materially different from distributions related to groups of patents that comprise narrower subsets of the broader technology. These studies also suggest that, for a given technology, patent value distributions have been relatively stable over time and may not be materially different across countries. This suggests that the results discussed above may be generalizable to a greater set of facts and circumstances than those fitting the data used in the individual studies. How much weight to give any given patent value distribution depends, however, upon the evidence in the case, including the nature of the patent portfolio being examined, what other information is known about the patents in the portfolio, and how the patent value distributions will be used. ■

Available at Social Science Research Network (SSRN): https://ssrn.com/abstract=3714864

Latest Articles Of The Month

Latest Articles Of The Month