If in 2021 the data created, captured, and replicated across the world is estimated at 80 zB, it should double in just four years to reach 170 zB in 2025. How big is that figure? Here is a simple insight: knowing that one zB (zettabyte) is one billion terabytes (1021), a regular personal internet connection would need more than 30,000,000 years to transmit a zettabyte. Because they are not comparable with common practices, such huge amounts of data are dealt with via dedicated infrastructures and Artificial Intelligence (AI) tools. Conversely, the development of AI fuels the need for more data.

In such perspective, there is an avenue for the development of digital markets. However, it will need to clarify how data creates economic value. Subsequent questions address at least two issues: 1) the measurement of data value, and 2) the process of valuation of data contribution to economic benefits. This article suggests some insights and building blocks. It develops in three parts. First, accepting that information- goods behave differently than non-information goods, we recall some specificities of data in the age of Artificial Intelligence. Second, we show that the application of common valuation methods to data, although not straightforward, is possible. Finally, in our third part we identify ways to operationalize data valuation methodologies.

1.1 New versus Old Data Processing

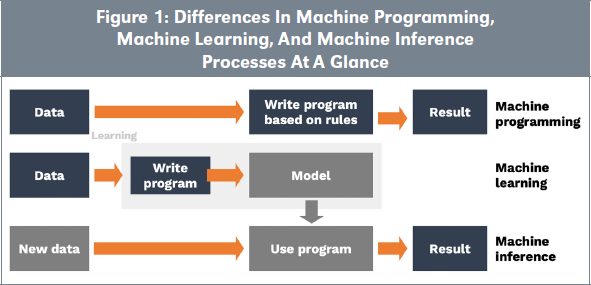

While data is used for machine inference and develops in volume, its relevance for the application of machine learning (ML) based solutions increases. Thus, while entering the age of AI, data usage also nurtures and supports the development of AI. This dramatically modifies data processing practices, and current data processing differs from traditional programming.

In traditional programming, code is written and then executed (Figure 1). In such context, the programmer keeps control on the code. The way data is used by AI fundamentally changes. In ML, selected or created models are trained on historical data; the operation is coined data feeding. The supervised or unsupervised ML algorithm reflects correlations and patterns of the data. This results in the creation of a model that can be used for further simulations or predictions on other data sets. Next, another data set applies the trained model and creates a predictive output, which is a new data set.

Two new features, absent in traditional programming, characterize this processing: 1) there is opacity about the actions conducted by the ML model, and 2) there is a significant dependency on the data that was used for training because, contrary to theory-derived models, data is embedded in the ML model construction (“data is the new code”). Concretely, the same operation run on a different data set will result in a different model. It follows that the relevance of the obtained results depends on both the quality of the ML model and of the data. Thus, data is part of the solution, and without data the solution is useless.

For these reasons, the development of AI addresses issues related to the value of the data used for training and validation as well as the value created by data while contributing to AI processes, or before its contribution. Those are IP and valuation issues that in practice usually remain unquestioned at the early testing and experimentations stages, as those are quite easy to run. However, they become prominent when one reaches a scaling stage.

1.2 New IP Challenges in the Era of AI

The following paragraphs roughly describe the AI data processing operation at the aforementioned stages: the training stage and the inference stage.

1.2.1 The Training Stage

At the training stage, an AI tool uses (mostly) big sets of historical data, likely combining public and proprietary data. This raises some issues. First, once used to train for machine learning, it becomes difficult to isolate the combined data out of the model. Second, out of the multiple feeding data sets, it is difficult to identify the contribution of a single data source to the model. Hence, some data sets or subsets could become significantly useful while others contribute only marginally. Third, since the data sets used for training require some preparation, the assessment of the effort put in the preparation is also a challenge.

Current usages suggest that data merged with domain knowledge for model design results in the most promising applications for businesses. Further, huge efforts in research are done to reduce the amount of data needed for training. Thus, there are paths for exploring optimized processes that will likely change the dependency on specific data, while increasing the relevance of pretrained models.

At that stage, data ownership issues are already manifold. For example, one could run a ML model thanks to licensed data. Several questions follow: 1) Who owns the data? 2) Can one lose ownership? 3) Is a revocation of access to data possible? And 4) If 2 or 3 occurs, how will this impact the trained model?

The clear identification of associated rights is relevant in that rights indicate where cash flows will be oriented once the AI model will generate economic benefits. Also, the use of proprietary data could diminish risks associated to data processing. Thus, risk assessment becomes a key operation in data sharing strategy. This would include gauging the vulnerability of the model to the structure of rights or, when data contains potentially differentiating information, gauging the vulnerability to the loss of competitive advantages. Indeed, similar to a recipe, most economic value depends on “secret ingredients” where one of the ingredients is data. It follows that managerial challenges will include 1) the identification of the data sets to collect and use, and 2) those that can be shared, but also 3) how it can be shared, whether by giving limited or unlimited access, and/or exclusive rights.

1.2.2 The Inference Stage

Similarly, at the inference stage there persists a high dependency to the provision of data. This is because the model runs on current data, often real time data, with as much contextual information as possible. It follows that without access to new data for further application, trained models remain useless. Moreover “updates” are conducted through retraining, therefore continuous access to the training data set is a condition for operation. Beyond data volume, data quality is also an issue. Example 1.3 in Insert 1 illustrates how much quality is critical to ensure the marketability of an AI system.

| Insert 1: Some Examples Of Data And ML Combined Applications |

|---|

| Example 1.1: Language Models and the Appropriate Training Data

GPT-3, a language model that uses deep learning to produce human-like texts, is trained on most data available on the Internet. Wu Dao 2.0, the largest and probably the most powerful neural network ever created, was trained on 4.9TB of text and graphic data in Chinese and English and counts 1.75 Billion parameters (https://towardsdatascience.com/gpt-3-scared-you-meet-wu-dao-2-0-a-monster- of-1-75-trillion-parameters-832cd83db484). OpenAI, the creator of GPT-3, has put much effort in selecting data of higher quality, which reduced the amount of training data but increased the value. Moreover, OpenAI applied the latest model architectures (attention-based transformers) and developed a self-supervised training process. Other actors working on language models argue that their models might be of higher quality because they rely on proprietary data of the highest quality. However, many doubt that the addition of high-quality proprietary data will increase the quality of the application compared to the approach of OpenAI that refined public data and combined them with innovations in the training process and model architecture. Example 1.2: Facial Recognition and the Legal Framework Clearview, an American facial recognition company, collected images through crawling social media platforms. This has become a highly controversial way of collecting as much data as possible and combined images of faces with all other information that is (or was) available. As a result, they created a unique asset by their approach to data collection and aggregation, which is combined with state-of-the-art computer vision algorithms. This asset is now at the core of the company’s solution. In many countries, there is an ongoing discussion about the legal status of the data collection. Example 1.3: Cancer Detection and the Quality of Data Annotation A report highlighted that the IBM Watson application for cancer detection was biased by those doctors who initially labeled the data. This suggests that recommendations for treatments could potentially be biased by those who built the systems. Aware of the pitfall, users little adopted the system. In that case, IBM’s strategy consisted in putting a high effort on labeling data with the help of specialists. But the system is only as good as the data it is fed with. Therefore, in its attempt to create a unique proprietary data set, bias in data quality significantly reduced the economic value of the solution. Indeed, the assessment of the quality of the data can be difficult if not impossible and it follows that the common hypothesis is that only a few experts are able to annotate data in such a manner that quality is assured. |

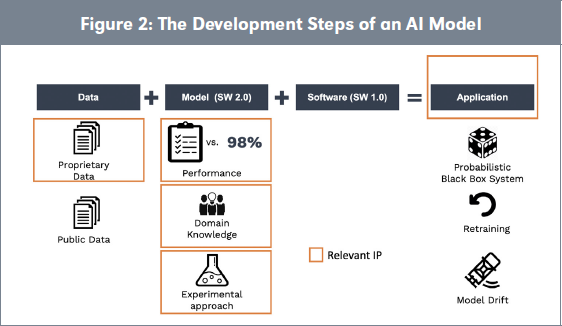

But data is not the only key input to produce a successful output of a training session. In addition to data, one has to define a suitable preprocessing and select the appropriate model that will achieve the highest level of accuracy. For example, in the field of autonomous vehicles, 98 percent of accuracy is not sufficient; the target is beyond 99.9 percent. Notably, the marginal progress of less than two points is conducted through experimentations and can take years as it often requires hundreds or even thousands of training runs before the model reaches the expected accuracy. Hence, it requires significant investment in time and workforce. Methodological choices made at that stage are potentially differentiating. The combination of domain knowledge and models are expected to result in the most stable and accurate output for the desired application. Finally, the model produces feedback loops that are fed by new data and that improve the model. In summary, the approach with which models are trained is a key enabler for faster and more reliable application development and can become a significant competitive advantage. This is significantly different than a traditional approach with a list of requirements one can work against. Ultimately, this results in unique and protectable applications combining data with traditional software (Software 1.0) as well as ML-based components (Software 2.0), where traditional software helps to bring the model to the field and make its usage intelligible.

Later on the application needs maintenance, but the update of the model cannot be conducted with a simple patch and the model needs retraining. As the environment is dynamic, the model becomes less and less accurate and one needs to actualize it. This is called model drift. It is a maintenance issue that requires monitoring because the available data is also evolving with respect to the initial feed data. Figure 2 illustrates the components of an AI application embedding data.

From an IP perspective the operations differ from traditional IP operations and raise several questions: 1) How relevant to the output is the new data? 2) Does it contribute more or less than initial data to the model? 3) What is the value of different data coming from different devices that run the same models? Those are currently unresolved accounting and fiscal issues yet to explore. There is also a question of ownership of the model that was developed on initial data and improved with the additional data (that potentially comes from different data owners). Orange rectangles in Figure 2 point to major IP issues in AI data processing.

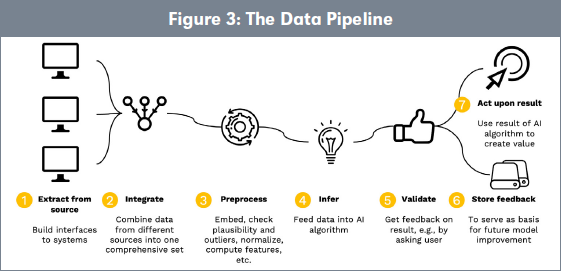

1.3 The Data Pipeline

An applied view on the same process suggests to distinguish seven steps in AI data processing (Figure 3), focused on data.

Step 1—Extract from the source: Especially in B2B contexts, suppliers of components but also Original Equipment Manufacturers (OEMs) struggle to access the required data during operations. There is a good reason for that: data is typically owned by those who produce the data during operation. Data market development and the enhancement of data value will be supported by an easier access to data.

Step 2—Data integration: This creates a situation with many different potential owners. From a legal perspective the situation is often fuzzy because, in the absence of regulations, it is not clear to what extent data can be used (e.g., car manufacturers vs. drivers; machine manufacturers vs. machine operators). As a default approach, contractual agreements define how data can be used by those who created the ML applications.

Step 3—Preprocessing: Moreover, data needs to be preprocessed and, e.g., correctness of data needs to be assured. If sensors send erroneous data, decisions by the ML system might be flawed or feedback loops do not work correctly. This becomes even more complicated if the system relies on data from other or multiple suppliers.

Consequently, data sources need not only deliver the specific information needed for the ML-based application but should also deliver contextual or labeled data allowing plausibility checks and quality control.

Step 4—Inference: This is when new data is needed to feed the algorithm and the same issues as those of Step 1 arise. Also, as aforementioned, the relative dependency of the model on the initial data set and the new data set is an issue.

Step 5—Validation step of the output: The application requires access to data to ensure the output of the solution makes sense.

Steps 6 and 7—Maintenance and value creation: Ultimately, due to changes in the environment model quality degrades, and the model has to be retrained. This requires access to the original data set for training in addition to the data collected in the meantime.

Consequently, original training data loses value over time while more recent data becomes more valuable. This suggests that the valuation of data follows a dynamic process that makes data value a characteristic that is relevant and valid on a short temporal window only. In any case, without access to the data during inference, the model is of significantly reduced value. Also, as pointed to before, in training and inference stages, data quality is most important for the successful application of AI.

Figure 3 sheds light on how data flows through the pipeline and how different this process is from traditional data processing.

As described in Part 1, data has to be exchanged and processed for ML-based applications to work. Therefore, it is essential to be able to share, sell, or purchase data. Surprisingly, despite the relevance of data sharing, the application of valuation methods to data is still scarce.

2.1 Valuation of Intangible Assets: Basic Methodologies

Intangible assets valuation is not different from the valuation of a company, especially now that intangibles represent 90 percent of enterprise values (Ocean Tomo, 2020). However, there are important differ ences between company and intangible valuations. In the first case, the legal framework is clear enough to delimit the scope of the valuation, whether a limited partnership or a newly created company. In the second case, valuators are less equipped when it comes to defining the limits of intangibles and moreover, of data. It follows that the first issue met by valuators is the definition of the valuation object. The first part of this article has offered a useful description of the pipeline to situate the object of valuation in the data processing pipeline. Indeed, valuation could alternatively focus on training data or the AI algorithm. As mentioned here before, and considering the short validity of a valuation, a second issue relates to the date of the valuation.

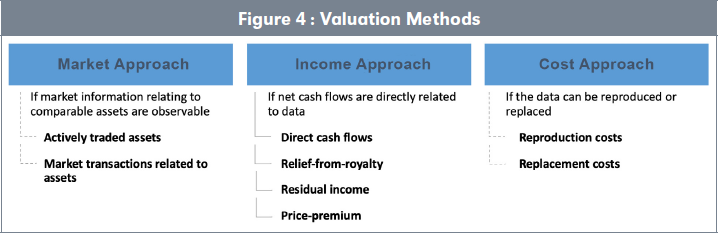

Overall, there are three accepted methods to value intangible assets (Figure 4). We describe them in the following paragraphs.

2.2 The Market Approach

This valuation approach derives a value from the observation of recent existing transactions of similar assets. This is the preferred fair value valuation according to the international financial reporting standard which defined a hierarchy of fair values in the dedicated standard IFRS 13. Preferably, transactions should be observed on a liquid market and involve an identical asset. This is a situation described as Level 1 in IFRS. This of course is not possible when we are valuing intangibles. If Level 1 fair value cannot apply, IFRS suggests moving to Level 2 fair value. Level 2 fair value is based on transactions occurring on less liquid markets but on identical goods or on liquid markets of similar goods. The two levels adopt a market approach that is very convenient and accurate to estimate the economic value of a tradeable good by sticking to the current trend. However, it is often irrelevant when the market is highly volatile and unfortunately hardly applies to data transactions, as markets are not yet liquid and by construction, intangibles are dissimilar. Nevertheless, data sets are traded, more likely with confidentiality, but it may occur that a company has access to relevant information and be able to build an ad hoc comparable.

When a comparable transaction occurs, the valuator needs to identify the appropriate indicator. Those vary depending on the nature of the data set: it could be a price per user or a price per image, a price per profile or a price per data set or list. The indicator is next applied to the valuated transaction. Often, the valuator can make some adjustments to correct for uneven accuracy or differences in exclusivity rights or lifetime of the data. See Insert 2.

| Insert 2: A Drivers Data Set Value With Application Of The Market Approach |

|---|

| Company Y wants to value a data set of driver trajectories and behaviors that records 10,000 individual entries. Company Y exchanges information with actors of the sector and learns that Company X, a competitor, has recently sold a data set of 2,000 individuals on a data exchange for the price of 660,000 €.

Assuming that the information about drivers is similar across the two data sets, a single profile has a comparable value of 330 €. This makes a global value of 3,300,000 € for Company Y’s data set. If Company Y’s data set contains 6,000 records of individuals as compared to the 5,000 in Company X’s set, and assuming that the data contains information as relevant as the 5,000 entries, the price could increase by 20% and reach 3,960,000 €. |

2.3 The Income or Revenue-Based Approach

The revenue-based approach derives the value of the asset from the future revenues that it is expected to generate. Revenues can be understood as a generic term that describes different sources: the cash flows, the residual income, the price premium, and the relief-from-royalty generated by the exploitation of the asset. In contrast to the market approach, in which the time perspective is the present, the revenue- based approach is forward-looking. This temporal orientation supposes that a reasonable business plan exists that narrates the manager’s vision. In IFRS, revenue-based income is also appropriate to estimate a Level 3 fair value, when Levels 1 and 2 cannot be applied. It is often coined “the entity-based approach” because it tells the story from the company’s point of view or expectations.

Amongst the different sub-approaches, the most commonly used one is that of the Discounted Cash Flows. It requires the estimation of the probable incremental cash that will be generated by the asset. As mentioned above, those flows can originate from different sources: royalty, incremental margins originating in sales increase, and/or cost savings. This applies to data that is licensed or data which treatment will allow to save costs or generate extra revenues, for example by attracting new customers. The main difficulty in the application of the approach is the identification of the part of revenues that is strictly related to the IP. A conceptual limit of the methodology lies in its deterministic approach: it pretends to predict a one-path revenues stream in the future, whereas possible revenues streams are manifold and subject to contingencies that are unpredictable. Therefore, a basic revenue-based methodology should be completed by capturing distributions of cash flows rather than a unique series of cash flows (See LESI IPV committee webinar on the topic). The recognition of a distribution of cash-flows/incomes provides a better representation of uncertainty that a basic revenue- based method tends to elude. An illustration of a revenue-based application is provided in Insert 3.

| Insert 3: A Drivers Data Set Value With Application Of The Revenue-Based Approach |

|---|

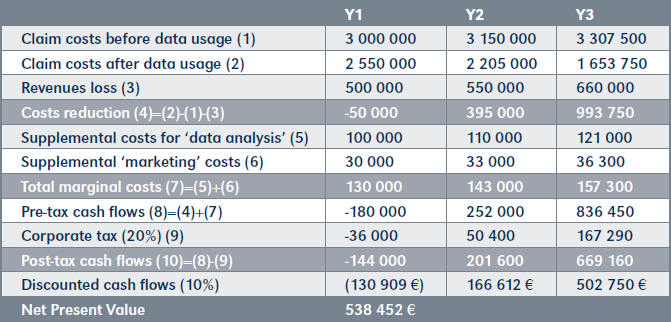

| The A Insurance Company wants to purchase the data set offered by Company Y because it contains drivers’ behaviors that could allow a new pricing strategy with premiums adjusted to predicted be-haviors. In order to assess the opportunity, Company Y builds a business plan including both the costs that it expects to save due to a decrease in claims and the revenues losses due to the withdrawal of customers whose premium price will increase. The decrease in both revenues and costs compose the expected yearly flows that will be subject to corporate tax. Post-tax flows are next discounted and summed up to form a value which is to be compared to the cost of investment. If the former is greater than the latter, the investment is deemed generating positive benefits to the company.

The table on page 162 illustrates such estimation (inspired by IMDA, 2019). First, the projection of cost of claims with and without data are compared. Losses in revenues are next deducted from the costs saved. Also deducted are the costs to manage the new data activity, which comprehends the salary of a data scientist who will update the model, and marketing costs for communicating about the company’s new strategy. Finally, tax payments are deducted to obtain cash flows. Cash flows are estimated and discounted to form a Net Present Value, which represents the current value of the data set. The NPV of half a million contrasts with the market approach result that was eight times greater. This is explained by the fact that a different usage is being valued. Concretely, the estimation can be multiplied as much as demand is sustained. |

Here before, we have observed that data (especially when used for ML applications) has specific characteristics that require an adaptation when one intends to use DCF methods. We call this a “data-value based valuation method.” In line with the DIN (Deutsches Institüt fur Normung) approach to patent value, an overall data- value factor is arguably a value that can be multiplied with the NPV value. A data value factor is composed of several dimensions, which can include:

The four factors evaluated in the ranges between 0 and 1 are complex and highly individual factors that are related to the assessed applications. They might also be part of the negotiation between customers and suppliers.

Why are factors depending on the application, and therefore, why is the value different? The application value can be assessed by the present value of all future cash flows that are expected from the specific usage at play. One specificity for learning systems regarding the application value is that the better the solution becomes over time —thanks to the feedback loop and the learning of the application —the higher the value over time. One illustration is that of a virtual assistant that becomes better in answering customer requests.

Similar to the DIN approach to patent value, the application value becomes a function of the dimensions assessment, with the following calculation:

(TV * CV * IV * DQ) * application value = value of data for a given application

Where application value is the discounted value of the cash flows generated by the application.

Moreover, if training and inference can be independent from each other, the overall value is equal to the sum of the training value and of the inference value. Training value includes the discounted value of the model used for other applications than the assessed one, while the inference value the sum of the assessed application(s). When inference matters, the sum of all applications is assessed as one trained model, which could be used in multiple devices or products. See Insert 4.

| Insert 4: A Multidimensional Data Valuation, A Simple Case |

|---|

| You want to build an AI-based sales support tool. With that aim, you are considering purchasing market data from a large market research organization. The sales revenues that the tool is expected to generate are 200,000 € per year, with an annual inflation rate of 2%. The project horizon is 10 years. In a world without tax and in the absence of costs, the project net present value is estimated to be 2 Million €.

But how can one assess the value of the data? First, one needs to define the contribution of the data to the tool. In the present case, the data component of the overall solution is thought to be 40% (20% for the model training and application development and 20% for the maintenance and ongoing retraining over the lifetime of the application). It follows that the data share is defined as 0.4. This coefficient reduces the NPV for the data to 800,000 €. Next, let’s consider the other dimensions of the data value. 1. Time Value: Knowing that market data changes over time, we assume that buying the data now will help the AI-powered sales support system to train well and to perform well as long as market dynamics do not change. Indeed, training data is historical data and is only valuable if it applies identically in the future. We predict that the market will change significantly every three-four years. Therefore, the purchase of three-year historical data means that annual data will have different validity times: one year of the oldest data, two years for the two-year-old data and three years of the latest data, i.e., a total of six years of validity. The required validity time for a three-year data series is 30 (3 * 10 years). Therefore, we estimate our validity duration to be 6/30 = 0.2. The maximum coefficient is reached every year when an updated data set is available for the past three years. 2. Contextual Value: The data that the market researchers collected contains most of the relevant content. You might have received a few more variables that you assume would have been relevant to better reflect the reality for your application, but you assume that it is almost complete. Consequently, the data contextual value is estimated to be 0.8. 3. Information Value: The data the market research organization offers is unique in the sense that no other organization offers this data. It is not substitutable. However, it could possibly be collected by other players because the data is accessible. Also, you are aware that the seller does not provide the data exclusively to you. Therefore, even though the value of the information is high, it is rather limited to the extent it costs someone else to collect and provide it. Moreover, the data set is only one of four very important data sets that you require for the application. Therefore, the IV is set to 0.2. 4. Data Quality: The data is granular and correct. However, there is a significant effort for your data engineers to check and correct it. Indeed, there is always the possibility that outliers exist due to mistakes made by the seller. The seller is indeed unable to guarantee error-free data sets. Consequently, you plan two weeks of engineering time, which costs you 20,000 €. Recognizing the cost and effort for quality control and quality improvement you set the DQ value to 0.2 The overall value of the data set is: 0.2*0.8*0.2*0.2* 800,000 = 5,120 € |

2.4 The Cost Approach

The cost approach approximates the data value with the costs of replacement or creation of a functionally equivalent data set. The practice is common in accounting and is the main approach used for assets’ first recognition. There is often a large experience in calculating costs associated to assets such as R&D costs or patents, and companies are equipped with managerial accounting measurements. Costs are often focused on the acquisition of rights, for example, a patent filing, and the related maintenance costs. In the case of data, a challenge will be to clearly identify and assess such costs.

The main limit of the method is obvious: there is little correlation between the costs incurred to create a data set and the value that it can possibly generate. Therefore, equating costs and values is a highly questionable approach. This is because the approach disregards the uniqueness or specific attractiveness of the data set. Also, the cost approach does not reflect the evolution of the environment and could be subject to time-lag effects. The replacement costs approach is a variant of the cost method that can circumvent the latter limit. This approach estimates the total investment expense that should be made in order to replace the data set. This value could be negligible when the data set is that of a large retailer’s customer behaviour, for example. However, the cost could be tremendous when the data to reconstitute is that which has been captured by a satellite or a telescope.

The cost approach adopts a retrospective temporal orientation when incurred costs form the value and adopts a forward-looking orientation when replacement costs are estimated. Thus, the interpretation of the two approaches differs as the incurred costs bears little or no risk of estimation, whereas replacement costs bear an estimation risk. See Insert 5.

| Insert 5: A Drivers Data Set Value with Application of the Cost Approach |

|---|

| Company Y has spent the following amounts of money to develop the data set:

Entry costs that include regulatory compliance, authorizations to collect data, the development of the sensor that will track the drivers’ behaviors, and the installation or provision of facilities to store the data. Overall, costs are estimated to be worth 2,000,000 €. This includes software and storage, but not the human capital and marketing costs already estimated in Insert 3. The latter and other costs incurred to create the data set amount to 2,500,000 €. Again, this value contrasts with the market- and revenue-based approaches but the meaning is different. The data set was worth 2.5 M€ of investment to Company Y because, in the long term, more benefits are expected to be generated from such investment. |

Some characteristics make data a particular economic object that challenges the assumptions and underpinnings of traditional valuation models, and which subsequently require some adaptations.

First, data is non-rival. As suggested in Insert 3, one kind of use does not hamper other usages. It follows that multiple sources of revenues can be envisaged, and amongst those, the multiple sales of a same data set or the multiple sale of different versions of the same data set (Shapiro & Varian, 1998).

Although data intrinsic value may vary in time (Fernandez et al., 2020 —Figure 4), it does not necessarily degrade by erosion or obsolescence; it may stay constant or even increase. For example, some cohorts of drivers could be more and more valuable with time be- cause they will allow a better understanding of drivers’ risky behaviors through ages and in relation to claims (i.e., incidents or accidents).

Contrary to common thinking, data remains an excludable good because the “holder” (data ownership does not exist) can specify usage modalities in a contractual agreement: it can be licensed, subject of a unique access, of multiple access, it can be reproduced or not, modified or not, sold or not, etcetera. The limit of excludability resides in the control that the holder can have on the data usages. Thus, another condition to excludability is the investment in cybersecurity and controls. Paradoxically, a vulnerable holder could be excludable from the data that he generated on his own. This implies that projected cash flows are conditional to the existence of such controls. See Figure 5.

Also, it may be worth recalling that, as with other goods, data value exists on the condition that it is used. Conversely, stored data has no direct economic value if the means of its exploitation are not invested in. Exploitation is in many ways similar to an investment decision and requires the estimation of cash flows or earnings. To do this, valuators model a business plan that captures the chain of activities that an organization performs in the aim of delivering valuable data usages. Therefore, it becomes relevant to understand the data value chain (DVC) to build the useful business plan.

In a DVC, information flow is described as a series of steps needed to generate value and useful insights from data (Curry, 2015). For example, how data is collected can be key to building a value proposal (Example 3). Also, data quality and integrity are issues and investments that secure those will maintain value. Because of their importance, the European Commission sees the DVC as the “centre of the future knowledge economy,” bringing the opportunities of the digital developments to the more traditional sectors (e.g., transport, financial services, health, manufacturing, retail)” (DG Connect, 2013). This raises the following question: Does a general consensus exist about what is a DVC? The answer is no, and anyone browsing the Internet will find a multiplicity of DVCs counting from four to sometimes 12 steps. We suggest a synthesis that matches the data pipeline introduced before (Figure 5). At each of the DVC stages, activities generate costs or revenues. To illustrate each step, we examine the case of Company G, a geolocation forecast provider. See Figure 6.

The steps are:

Company G can either invest in installations capturing the necessary data or buy it from actors specialized in data capture. In the latter case, G can turn to the few oligopolists in the domain or buy data on existing market places (Dawex, aws, snowflake…). Knowledge on data price fixation is still scarce, therefore procurement solutions could vary highly from one solution to the other and from one seller to the other.

As a geolocation data treatment entity, G deals with geolocation data that sometimes is labeled accordingly with the means of transportation (by foot, by car, by bus, etcetera) or alternatively, is not. In the latter case, to build a geolocation forecast, G will need to label the data by conducting some reverse engineering. This has a cost that will add to the purchase price of data and, moreover, this slightly increases risks due to inference bias.

G’s machine-guided or men-guided process consumes energy and time. Managerial choices described in the first section can significantly impact the P&L.

G manipulates data thanks to its workforce and an AI component. This supposes IP protection costs, AI development costs, and cybersecurity costs.

G will expense advertisement costs for geolocation services, communication costs in specialized forums, of registration on platforms, etcetera.

Geolocation data can be useful in the situation of a pandemic for car makers because traffic information will support their inventory management. The effective usage can substantially differ from the reason why data was created in the first place. As a consequence, the potentially generated revenues are multiple and difficult to forecast.

In the end, the condition for determining the value of data is, more than for any other asset/good, the existence of a view of the upcoming usages.

AI applications are special, which significantly drives the value of data and the need for proper valuation techniques. After highlighting the unique aspects of data in ML-based applications, we have shown that the three traditional approaches to IP valuation can apply to data valuation cases.

The market approach has currently little relevance, but the expected development of data exchanges might evolve towards a more liquid market and better price predictability.

The cost approach is adequate to describe the investment made by the company producing the data, but it suffers from challenges when economic benefits are to be valued. This is because data can be used in multiple applications, which would decrease the cost for each individual case.

Revenue-based values are most complex to build as they require detailed business plans. They are considered as the most reliable and flexible existing solution.

Finally, we suggest that an ad hoc description of the DVC will support the work of the valuator in the financial modeling of projected cash flows. This will include technical development of AI as well as training and inference aspects.

Available at Social Science Research Network (SSRN): https://ssrn.com/abstract=4179547.

E. Curry, “The Big Data Value Chain: Definitions, Concepts, and Theoretical Approaches,” (2015). 10.1007/978-3-319-21569-3_3.

DG Connect, “A European strategy on the data value chain,” (2013).

T. Fernandez, N. Rivera, W. Xu, A. Gretton, “Kernelized stein discrepancy tests of goodness-of-fit for time-to-event data.” In International Conference on Machine Learning, (2020) : 3112-3122.

Infocomm and Media Development Authority (IMDA), Personal Data Protection Commission (PDPC), & Intellectual Property Office Of Singapore. “Guide to data valuation for data sharing,” (2019), p. 42. Retrieved from https://www2.imda.gov.sg/AI-and-Data.

Ocean Tomo, “Intangible-asset-market-value-study,” (2021). Retrieved from: https://www.oceantomo.com/ intangible-asset-market-value-study/.

C. Shapiro, H.R. Varian, S. Carl “Information rules: A strategic guide to the network economy.” Harvard Business Press, (1998).

Latest Articles Of The Month

Latest Articles Of The Month