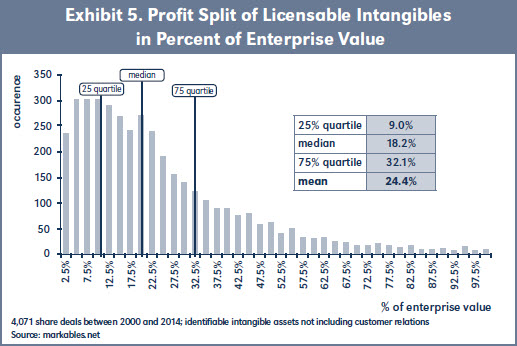

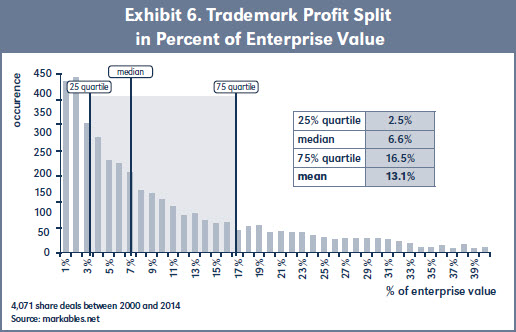

Purchase accounting data is helpful to gain a deep understanding of the transaction values of intangible assets, and their expected contribution to future prof-its of the acquired businesses. Such data is helpful to reconcile and redirect the profit-split method which has long been an important method for valuing intangible assets. With ample purchase accounting data available as comparables in the public domain, in-depth case-specific peer group analyses become possible. This will not only improve the quality of the profit-split method itself, but also make an important contribution to the overall accuracy of the valuation of intangibles in general.

*This article is based on an earlier version published in Valuation Strategies, Vol. 14, July-August 2015, and reprinted with permission.

- Uniloc USA, Inc. v. Microsoft Corp., 632 F.3d 1292, (CA-F.C., 2011).

- Gordon Smith and Russell Parr: Valuation of Intellectual Property and Intangible Assets, 3rd ed. (John Wiley & Sons, 2000) pages 401- 403; Emmanuel Llinares and Nihan Mert Beydilli: “How to Determine Trade Marks Royalties,” International Tax Review12 (December 2006) pages 29-30; Mark Zyla: Fair Value Measurement: Practical Guidance and Implementation, 2nd ed. (John Wiley & Sons 2012), pages 288-293; Robert Reilly and Robert Schweihs, Guide to Intangible Asset Valuation (AICPA 2013) pages 311-312.

- For a detailed description see Robert Goldscheider: “The Classic 25 percent Rule and The Art of Intellectual Property Licensing,” 46 les Nouvelles 148 (September 2011), pages 151-153.

- Uniloc USA, Inc. v. Microsoft Corp., 632 F.3d 1292, (CA-F.C., 2011), page 1055.

- Or more, depending on the required return rates on tangibles and intangibles.

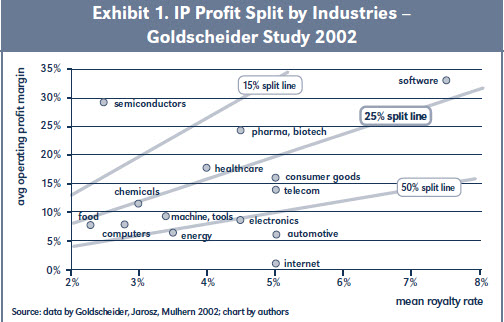

- Robert Goldscheider, John Jarosz and Carla Mulhern, “Use Of The 25 Percent Rule in Valuing IP,” 37 les Nouvelles 123 (December 2002).

- Using data from successful licensees only.

- This range does not include the media and entertainment and the internet industry. Here, long-term industry profitability as far below median royalty rates, resulting in flawed ratios.

- Jonathan Kemmerer and Jiaqing Lu, “Profitability and Royalty Rates Across Industries: Some Preliminary Evidence,” 8 Journal of the Academy of Business and Economics (March 2008).

- Jiaqing Lu, “The 25 Percent Rule Still Rules–New Evidence from Pro Forma Analysis in Royalty Rates,” 46 les Nouvelles (March 2011).

- 25/100 versus 25/(100+25).

- A detailed discussion of the empirical tests was published by Douglas Kidder and Vincent O’Brien, “Simply Wrong: The 25 Percent Rule Examined,” 46 les Nouvelles 263 (December 2011).

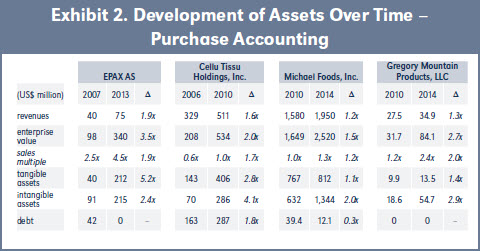

- Norwegian EPAX AS, a supplier of Omega-3 fish oils, was acquired in 2007 by Austevoll Seafood ASA, and then in 2013 by FMC Corporation. Cellu Tissu is a manufacturer of specialty tissue paper for use in personal hygiene products. Cellu Tissu was acquired in 2006 by Weston Presidio (an investment firm), and in 2010 by Clearwater Paper. Michael Foods is a supplier of specialized egg and potato products to retail and food service. It was acquired in 2010 by Goldman Sachs, and again in 2014 by Post Holdings. Gregory Mountain Products is a leader in technical backpacks for climbing and hiking. It was acquired in 2010 by Clarus and combined with Black Diamond Equipment, and in 2014 by Samsonite.

- MARKABLES is a database containing data from over 7,500 PPAs, with a particular focus on trademark and brand assets. www.markables.net.

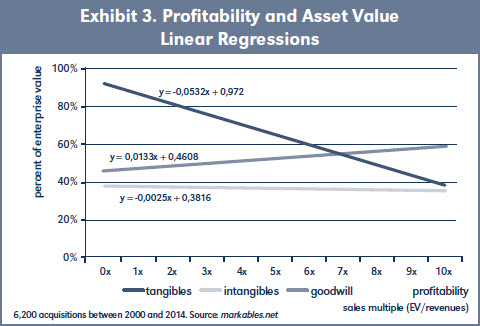

- The three lines do add up to more than 100 percent due to non-interest bearing liabilities. Such liabilities decrease with increasing profitability.

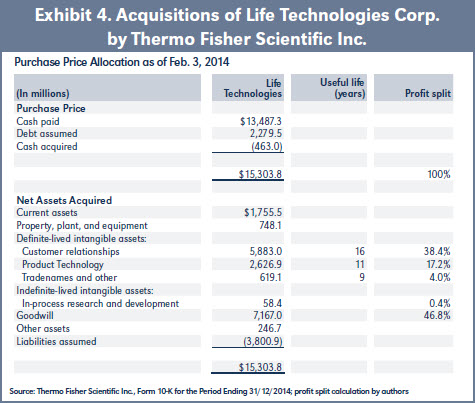

- 17.2 percent + 4.0 percent + 0.4 percent = 21.6 percent

- For a comprehensive and detailed overview of fair value accounting, see Mark Zyla: Fair Value Measurement: Practical Guidance and Implementation, 2nd ed. (John Wiley & Sons 2012).

- See Paul Komiak, “Control Premiums: Evidence against market integration,” in: 3 Journal of Business Valuation and Economic Loss Analysis (January 2010).

- MARKABLES is a database containing data from over 7,500 PPAs, with a particular focus on trademark and brand assets. www.markables.net.

- Ednaldo Silva, “Letter in Reply to OECD on Transfer Pricing Comparability Data and Developing Countries,” April 11, 2014. Accessed at http://www.oecd.org/ctp/transfer-pricing/ royaltystatllc-conparability-and-developing-countries.pdf.

- The graph is cut at 40 percent.